Why Wallet Identity Becomes the Backbone of On-Chain Finance — and Where VerifiedHub Fits

On-chain finance is no longer a thesis. It is plumbing. Treasuries, money-market funds, private credit, and tokenized equities are already settling on public ledgers, and the legal scaffolding around them is hardening month by month. But as the rails mature, a quieter problem keeps surfacing — the same one that surfaces in almost every BitVision story about tokenized markets. We have built systems that can move value at internet speed. We have not yet built systems that can answer a simpler question: who is on the other end of this wallet?

This is the question OnFi cannot route around. And it is the reason wallet identity verification is about to stop being a compliance afterthought and become the load-bearing layer of the entire stack.

1. What OnFi Actually Is

OnFi is not simply institutional DeFi. It is what happens when the core functions of traditional finance — issuance, trading, custody, transfer, clearing, settlement, compliance, collateral, financing, and global distribution — are rebuilt on blockchain rails.

Early DeFi was largely crypto-native: tokens trading against tokens. OnFi is different in scope. It asks how real assets — securities, stablecoins, tokenized stocks, funds, government bonds, network tokens, and digital goods — can be issued, distributed, priced, and settled on-chain. When properly understood, OnFi is a new distribution layer for the global financial market.

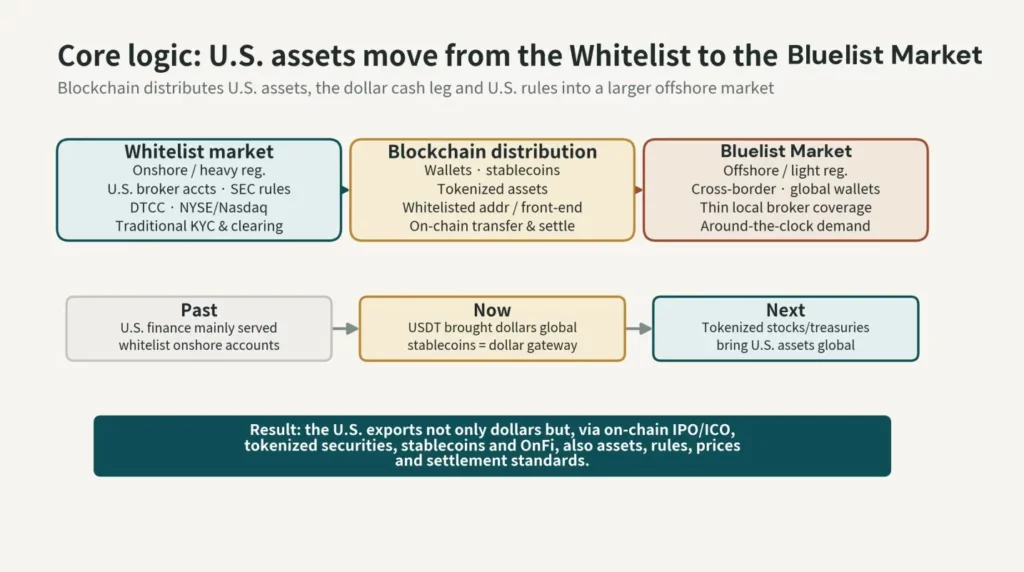

That distribution layer reaches two very different audiences. The whitelist market is highly regulated, onshore, KYC-bound, and account-based — the world of brokerages, banks, custodians, and licensed exchanges. The blue-list market is the larger cross-border audience that has genuine demand for U.S. assets but is outside the reach of traditional brokerage and bank account coverage.

The blue-list market is not lawless, nor is it synonymous with illicit activity. It is simply where traditional financial services are thin but real demand is thick. Wallet-native distribution, stablecoin settlement, and tokenized asset access are uniquely suited to serve it. The strategic conclusion writes itself: U.S. assets need to serve the whitelist and bluelist markets simultaneously, and on-chain channels are the only rails positioned to reach both.

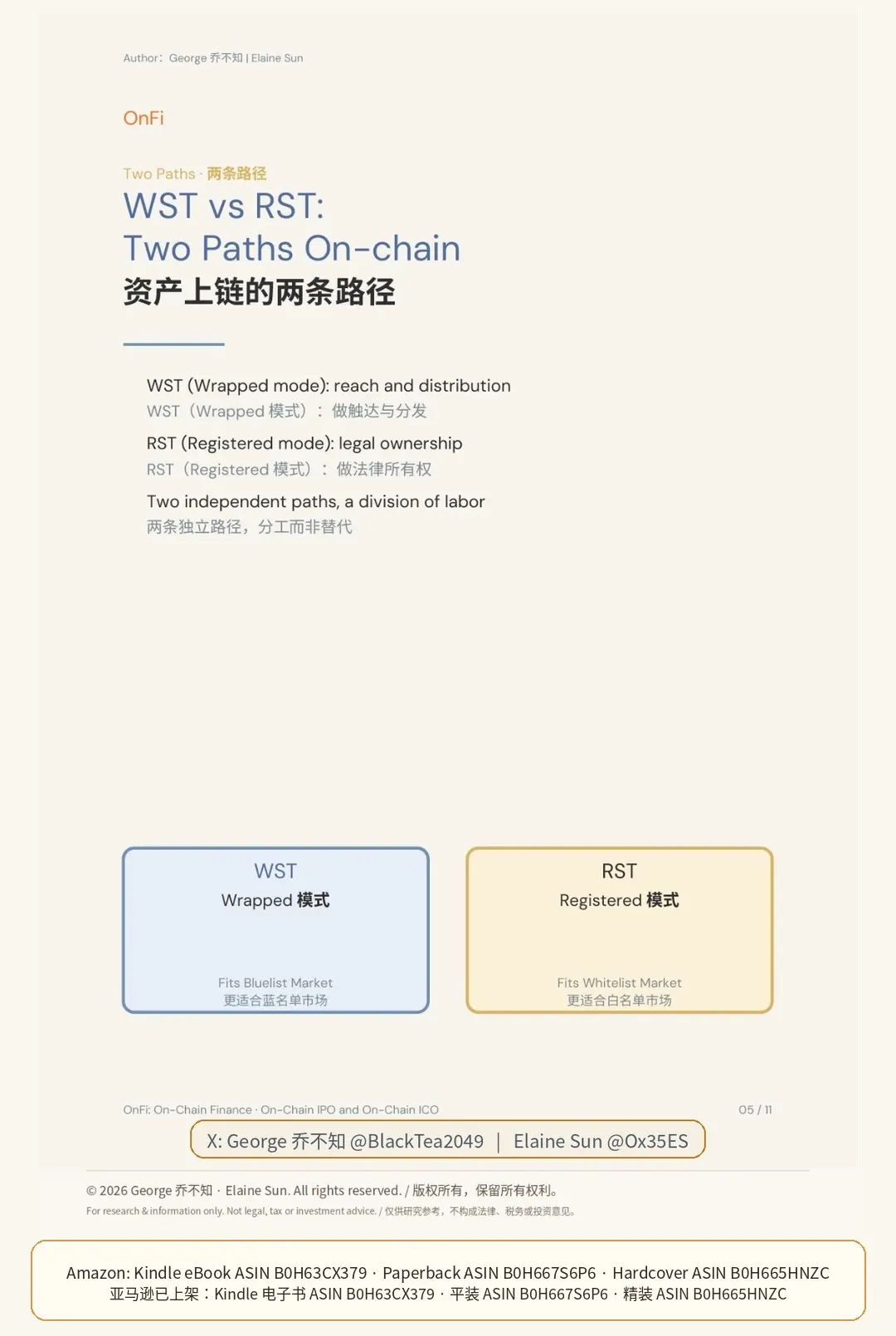

Tokenization itself splits along two paths. The Wrapped model (WST) issues on-chain tokens against off-chain holdings — fast to launch, strong at distribution, easy to compose with DeFi, but typically delivering economic exposure rather than full registered-shareholder rights. The Registered model (RST) anchors legal ownership through issuer-side registration, aiming for a world where token transfer is ownership transfer. WST maximizes reach; RST anchors rights. The future is not one replacing the other — it is coexistence, where each form must disclose, honestly, exactly what rights it confers.

Every one of these paths — whitelist or bluelist, wrapped or registered — eventually runs into the same wall: a transfer is only as trustworthy as the identities on either side.

2. The Legal Landscape Is Forcing the Identity Question

For years, on-chain identity was treated as optional — a feature you could bolt on later. The 2025–2026 legal cycle quietly ended that debate. Three developments matter most.

The GENIUS Act made stablecoins a regulated instrument.

Signed into law on July 18, 2025, the GENIUS Act became the first major U.S. crypto statute. It brought payment-stablecoin issuance under federal oversight, required 1:1 high-quality liquid reserves, and explicitly carved out stablecoins from securities and commodities treatment. Critically, it banned interest or yield on payment stablecoins. That single restriction is redirecting institutional capital out of idle stablecoins and into yield-bearing tokenized real-world assets — Treasuries, money-market funds, and private credit — a market that already reached roughly $26 billion in 2025. The settlement layer of OnFi now has a rulebook, and that rulebook assumes regulated issuers know their counterparties.

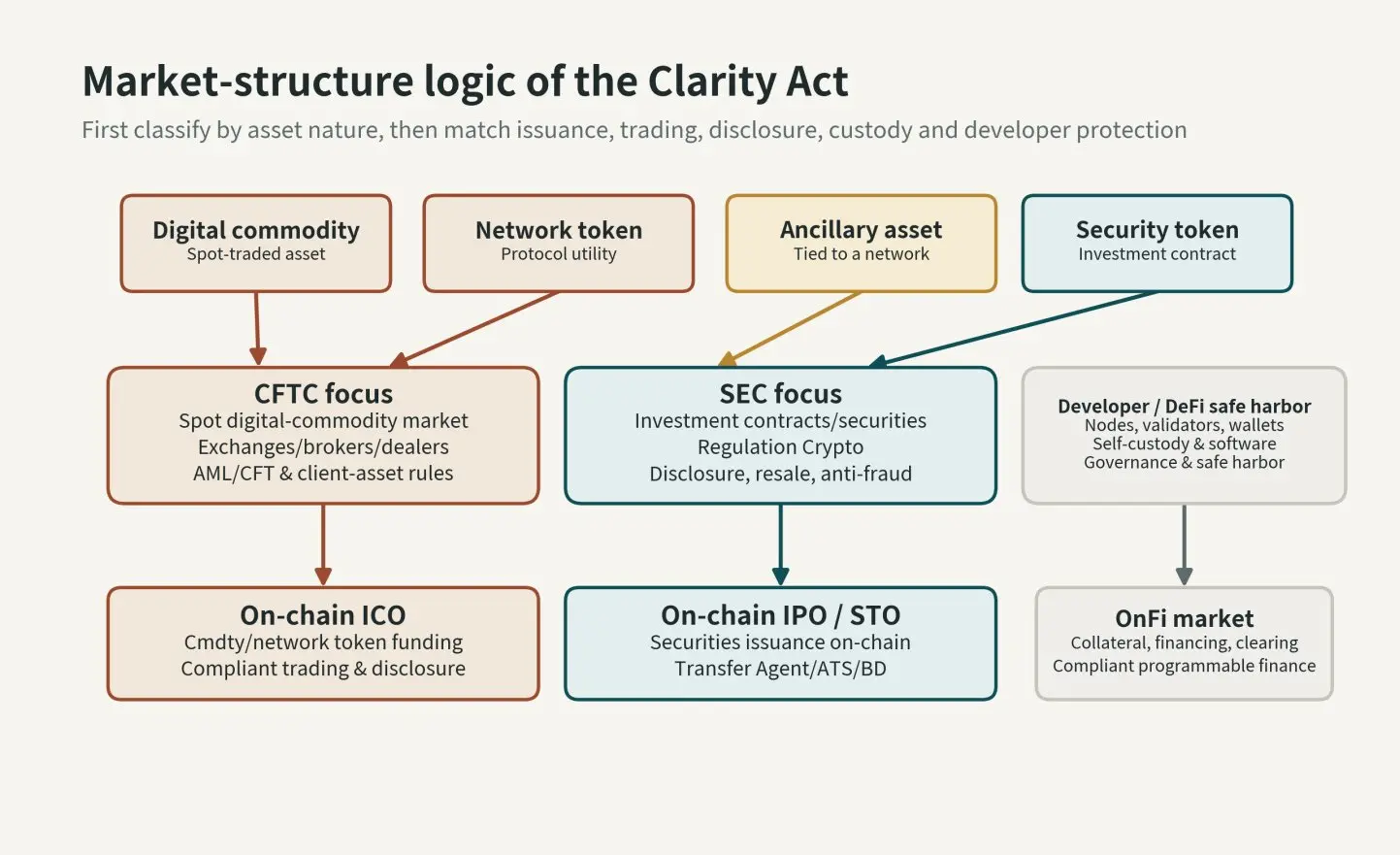

The CLARITY Act is drawing the jurisdictional map.

The Digital Asset Market Clarity Act (H.R. 3633) is the structural complement. As of June 1, 2026, it sits on the Senate Legislative Calendar under General Orders (Calendar No. 423) after the Senate Banking Committee advanced its version on May 14, 2026 — it is not yet law and still must be reconciled, clear a 60-vote floor, and be signed. But its direction is clear. It grants the CFTC exclusive jurisdiction over digital-commodity spot markets while preserving SEC authority over investment-contract assets, and it sets out a lifecycle path for projects — disclosure, financing limits, resale restrictions, exchange certification, and decentralization testing — alongside explicit illicit-finance provisions and protections for non-custodial developers.

Read carefully: CLARITY does something subtle: it pushes token issuance toward clearer classifications, stronger disclosure, and more disciplined market structure. A market structured that way cannot run on anonymous wallets. Disclosure obligations and resale restrictions only mean something if you can identify who is buying, holding, and reselling.

The compliance perimeter went global and biometric.

Outside the U.S., the FATF Travel Rule (Recommendation 16) now applies to virtual-asset transfers in 85 of 117 jurisdictions, up from 65 in 2024, with a USD/EUR 1,000 de minimis threshold, above which the originator and beneficiary identities must travel with the transaction. FATF’s June 2025 update strengthened originator-identity assurance to the point where biometric verification is becoming a practical necessity rather than a nice-to-have. In parallel, MiCA requires full CASP authorization across the EU by July 1, 2026.

The legal landscape of 2026 doesn’t ask whether wallets should carry verified identity. It assumes they already do — and penalizes the systems that pretend otherwise.

3. Why Wallet Verification Becomes the Load-Bearing Layer

Put the pieces together, and a clear architecture emerges. Compliance obligations in OnFi are split into two tiers: issuer-level and exchange-level. Increasingly, the asset itself is expected to enforce transfer restrictions — a tokenized security should not be able to move to a sanctioned wallet in the first place. That is only possible if wallets carry verifiable, machine-readable trust attributes.

This is exactly where on-chain IPOs hit their hardest problem. The frontier challenge is not price exposure — wrapped tokens already solve that. The challenge is making an on-chain transfer equal a legal transfer of ownership. Transfer agents, issuers, DTC participants, ATSs, custodians, brokers, and blockchain infrastructure must all agree on one thing before ownership can move: the identity behind the receiving wallet. No verified identity, no legal transfer.

The same logic governs prime brokerage as it transitions into OnFi. Future brokers won’t just provide accounts — they become the entry point to on-chain markets, and they must decide which assets can be displayed, traded, custodied, financed, or pledged as collateral. Every one of those decisions is downstream of a verified counterparty. And the bluelist opportunity — the cross-border demand that traditional banking can’t reach — only becomes addressable if wallet-native distribution can carry trust without a bank account attached.

So wallet identity is not a feature of OnFi. It is the precondition for almost everything OnFi promises: legal ownership transfer, regulated distribution, collateralization, and cross-border reach.

4. Verification Without Surveillance

Here is the tension. The naive answer — publish full identity data on-chain — would destroy the very properties that make on-chain finance valuable: privacy, composability, and global access. A public ledger of everyone’s passport is not progress.

The 2026 toolkit resolves this. Zero-knowledge proofs can confirm that a wallet is sanctions-free or has passed a KYC check without revealing the underlying personal data. Verifiable credentials issued by trusted parties can be selectively disclosed. Soulbound tokens can represent eligibility or compliance status that travels with the wallet but exposes nothing private. The goal is recognition, not exposure — proving that a wallet is trustworthy without broadcasting who stands behind it.

The next generation of digital identity is not a database of names. It is a portable, privacy-preserving proof that a wallet has earned the right to act.

5. VerifiedHub: A Recognition Layer for the Next Generation of Identity

This is the gap VerifiedHub is built to fill. If OnFi is the distribution layer for global finance, VerifiedHub is the recognition layer that sits beneath it — the place where a wallet, a domain, and a public profile become a single, verifiable identity that other systems can trust.

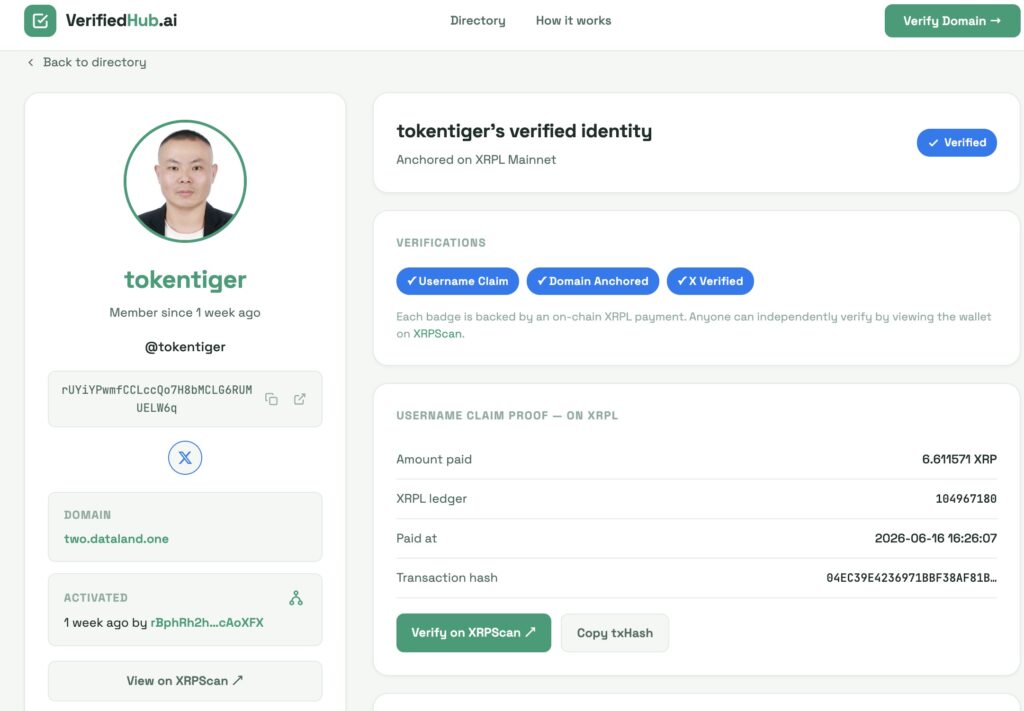

The approach is deliberately different from legacy onboarding. VerifiedHub does not run KYC checks on documents, collect passports, or store personal data. Instead, it uses well-established cryptographic methods to prove the only thing that actually matters on-chain: control and ownership. A counterparty proves they control a wallet by signing a challenge with their private key, and they prove they control a domain by publishing a matching attestation at a well-known location on that domain. Bind the two together, and you have a verified wallet-domain pair — a cryptographic statement that the entity behind this address is the same entity behind this web presence. Extend the same method to a public X account, and the wallet now carries a portable proof of who controls it, without anyone ever having to hand over an ID.

Anchoring that credential on the XRP Ledger is a natural fit. The XRPL is already where regulated, real-money settlement is happening rather than meme-driven speculation — fast, low-cost, deterministic finality, and a built-in orientation toward institutional and cross-border use. A verification layer needs exactly those properties: cheap enough to verify at scale, final enough to rely on, and neutral enough for any issuer, broker, or counterparty to check.

The result is a chain of trust that runs from a verified domain to a verified wallet to a settled on-chain transaction — anchored entirely in proof of ownership rather than disclosure of identity. Nothing private ever touches the public ledger. What travels is the proof, not the person — and because the methods are open and well-known, any issuer, broker, or counterparty can verify the pairing themselves rather than taking a third party’s word for it.

That is what building trust for the next generation of digital identities actually means in practice. Not a walled garden, and not a surveillance database — a portable, privacy-preserving proof of standing that lets the whitelist and bluelist markets transact with each other on rails everyone can audit. The Bottom Line

OnFi will win the same way the internet won — by becoming infrastructure that fades into the background. But infrastructure has to be trusted before it can disappear. The GENIUS Act regulated the money. The CLARITY Act is structuring the market. FATF and MiCA drew the global perimeter. Every one of those frameworks quietly assumes a layer that does not yet exist at scale: a way to know and prove who is behind a wallet — without giving up the openness that made on-chain finance worth building.

That layer is the real frontier. Tokenization solved how value moves. Verification is how value learns who to trust. VerifiedHub is a bet that the next trillion dollars of on-chain finance won’t be unlocked by faster settlement or cheaper gas — it will be unlocked by identity that finally travels as well as the assets do.

Disclosure & sources

This article is editorial commentary, not legal, investment, or financial advice. The CLARITY Act had not been enacted as of publication and remained subject to Senate action. Key references: GENIUS Act (Sidley, Richmond Fed); Digital Asset Market Clarity Act, H.R. 3633 (Congress.gov; Davis Wright Tremaine); FATF Travel Rule / Recommendation 16 and MiCA timeline (Sumsub); on-chain privacy & compliance tooling (TRM Labs, Chainlink); RWA market data (Chainalysis).